What is Step-Up SIP vs Regular SIP?

A Regular SIP invests a fixed amount every month throughout the investment period. A Step Up SIP increases the investment amount every year by a fixed percentage, usually aligned with salary growth. This small change significantly increases long-term wealth because higher contributions enter the market at different stages of compounding, boosting total returns over time.

Why Step-Up SIP creates more wealth

Step-Up SIP works on a simple principle: income increases over time, so investments should also increase. Instead of investing the same ₹ amount every month, you increase it yearly.

This creates:

- higher total capital invested

- stronger compounding effect

- better alignment with salary growth

Platforms like Groww, Zerodha Coin, and Kuvera actively promote step-up SIPs because they improve long-term investor outcomes.

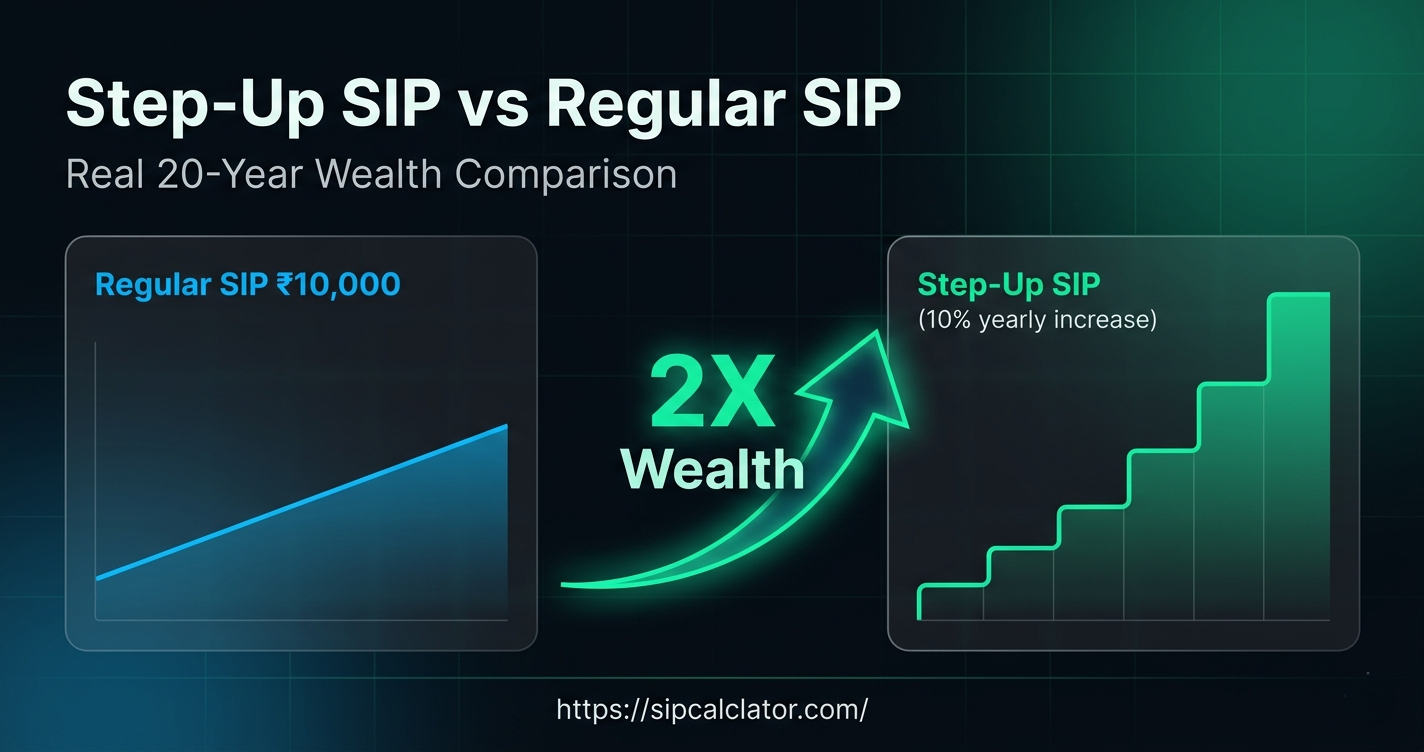

Real comparison: Step-Up SIP vs Regular SIP (20 Years)

Let’s assume:

- Monthly SIP: ₹10,000

- Duration: 20 years

- Expected return: 12%

Regular SIP

- Monthly investment: ₹10,000 fixed

- Total invested: ₹24,00,000

- Final corpus: ₹99.9 lakhs

Step-Up SIP (10% yearly increase)

- Starts: ₹10,000/month

- Annual increase: 10%

- Total invested: ₹68.7 lakhs

- Final corpus: ₹1.89 crore

👉 That’s almost 2X wealth creation with the same discipline, just smarter structure.

Why Step-Up SIP performs better

Step-Up SIP benefits from:

- higher investment base every year

- improved rupee cost averaging

- stronger compounding in later years

- salary-linked contribution growth

In long-term equity investing, later years matter the most because money has more time to compound aggressively.

What is a good step-up percentage?

Most investors use:

- 5% → conservative

- 10% → optimal (salary-linked growth)

- 15% → aggressive (high income growth)

Even a 10% step-up can significantly outperform a flat SIP over 15–20 years.

Step-Up SIP vs Regular SIP behavior over time

| Factor | Regular SIP | Step-Up SIP |

|---|---|---|

| Monthly investment | Fixed | Increasing yearly |

| Total invested | Lower | Higher |

| Wealth outcome | Moderate | High |

| Salary alignment | No | Yes |

| Long-term compounding | Standard | Accelerated |

How Step-Up SIP works in real investing

Step-Up SIP is supported by major platforms like:

- Groww

- Zerodha Coin

- Kuvera

It uses NAV-based mutual fund investments and applies XIRR to calculate actual returns over time.

The key idea is simple:

👉 higher contributions in later years multiply compounding effect significantly.

Is Step-Up SIP worth it?

Yes, especially for salaried professionals.

Because:

- income increases yearly

- inflation reduces purchasing power

- investment discipline improves automatically

Even a small step-up of 5–10% creates a massive difference in long-term wealth.

Internal linking insight

If you want to calculate your own investment growth, you can use this Step-Up SIP Calculator to compare different annual increase scenarios.

For basic projections, you can also try the SIP Calculator to estimate regular SIP returns.

FAQs

1. What is the difference between Step-Up SIP and Regular SIP?

Regular SIP invests a fixed amount monthly, while Step-Up SIP increases the investment amount every year. This allows higher compounding over time and better alignment with income growth.

2. How much more does Step-Up SIP give?

In most long-term scenarios, Step-Up SIP can generate 1.5X to 2X more wealth compared to a regular SIP due to increasing investment contributions and stronger compounding.

3. What is a good Step-Up percentage?

A 10% annual increase is considered optimal for most salaried investors. It balances income growth and affordability while maximizing long-term returns.

4. Is Step-Up SIP worth it?

Yes. It helps increase investments gradually without financial pressure and significantly improves long-term wealth creation compared to fixed SIPs.

5. Can I set up Step-Up SIP on Groww?

Yes. Platforms like Groww, Zerodha Coin, and Kuvera allow investors to enable Step-Up SIP options while setting up mutual fund investments.

Disclaimer

This article is for educational purposes only. Mutual fund investments are subject to market risk. Returns may vary based on market conditions, expense ratios, and fund performance.